SWIFT Last Dance?

The network that ruled global money flows for fifty years faces its final test: surviving programmable settlement.

For half a century, SWIFT has been the backbone of international payments. The name carries institutional prestige and the aura of neutrality. But what it really does is send messages, not money.

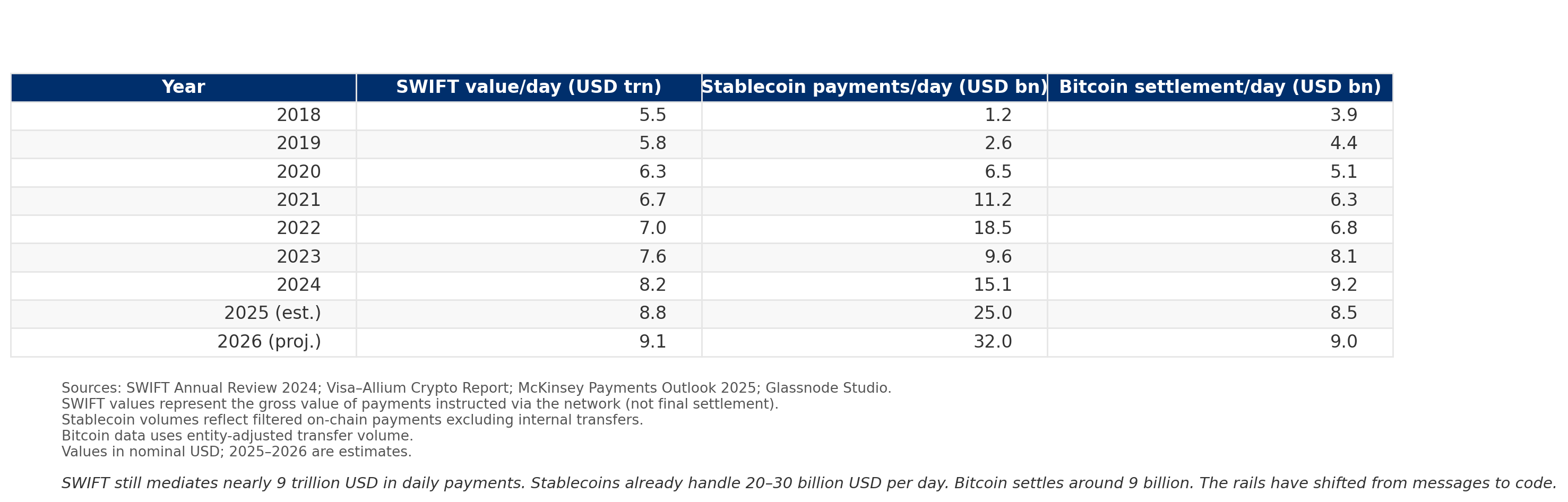

Every transaction depends on correspondent banks, time zones, holidays, and layers of human verification. In 2025, the network links more than 11,500 institutions, across roughly 40,000 payment routes, processing about 53 million messages per day.

It is vast, not fast.

Even SWIFT admits its delay. The forced migration to the ISO 20022 standard, with the end of coexistence with legacy MT codes on November 22, 2025, represents an effort to look modern.

The problem is structural. Standardizing the message does not change the fact that settlement still happens elsewhere. Money continues to move at the speed of banking bureaucracy.

SWIFT’s power is not in efficiency but in inertia. Banks and corporations profit from the intermediation and resist any replacement. It is a system protected by the very complexity it created. Technology has already shifted scale, but the protocol has not. SWIFT is a typewriter in the age of smartphones. It still reigns, but it no longer rules.

The unauthorized digital dollar

While SWIFT struggles to modernize its messaging standard, a parallel system already performs the task it was built for: transferring value globally, directly, and in real time.

Stablecoins began as a workaround for crypto traders, but have become the unauthorized digital dollar. In 2025, their total market capitalization jumped from about 205 billion dollars in January to over 300 billion by October, according to aggregated market data.

The mechanism is simple and powerful. Each token represents a dollar held in reserve, mostly in T-bills and cash, and can move across borders 24 hours a day, 7 days a week, with no correspondent banks or clearing delays.

The pair USDT and USDC dominates the market, with a combined share between 80 and 82 percent. Institutional investors use them for hedging and settlement. Retail users in emerging markets use them to dollarize savings. Traders use them for instant liquidity between exchanges.

Everyone uses the same infrastructure, and no one needs permission.

The projections show the scale of disruption. Citi expects 1.9 trillion dollars in base capitalization by 2030, possibly reaching 4 trillion in an optimistic case. JPMorgan sees 2 trillion by 2028. Visa places the range between 0.5 and 3.7 trillion, estimating that around 90 percent will remain dollar-denominated.

Global liquidity is beginning to flow outside the banking system. Each tokenized dollar acts as an autonomous unit of financial infrastructure. It is the opposite of SWIFT, it doesn’t need messages, only code.

The new power: those who issue, finance

Stablecoins are no longer just instruments of liquidity. They have become a silent fiscal mechanism.

Every token issued represents a dollar in custody, and that dollar is almost always invested in U.S. Treasury bills. The result is structural. Stablecoin issuers have become financiers of the very entity that issues the dollar itself.

The process is automatic. As market demand for stablecoins grows, more T-bills are purchased to maintain reserves.

Tether and Circle, the issuers of USDT and USDC, have turned into significant institutional investors in the short-term debt market. Independent estimates point to tens of billions of dollars in Treasury exposure.

This flow creates permanent demand for short-dated paper and helps suppress rollover costs for the U.S. Treasury.

The macro effect is clear. Tokenized liquidity pushes short-term yields lower, facilitates refinancing, and masks fiscal imbalance.

The dollar remains cheap not only through monetary policy but through digitized private demand. Blockchain has become an arm of U.S. public finance.

The strength carries its own risk. A loss of confidence in issuers could trigger forced selling of T-bills, pushing yields higher and shaking markets. But as long as the flow continues, the Treasury has found a new buyer and that buyer does not use SWIFT, nor ask for permission.

The race for digital sovereignty

Governments were slow to react. When they finally understood the rise of stablecoins, they realized that the private digital dollar was already circulating at global scale.

The response came in the form of sovereign digital currencies, or CBDCs. The promise is to restore monetary control with state-backed technology. The problem is time. Bureaucracy never beats code.

In the European Union, the digital euro project remains in its preparatory phase until October 2025, with a potential budget exceeding one billion euros.

The goal is explicit: reduce dependence on American networks and respond to tokenized dollarization. The European Central Bank talks about integration with banks and fintechs, but the system still moves through regulators, committees, and procurement rounds.

China is ahead. The e-CNY is already functional for domestic retail use and has begun cross-border expansion through Hong Kong.

In September 2025, Beijing launched an international center in Shanghai, strengthening CIPS as an alternative to SWIFT. It shows that monetary sovereignty has become a tool of geopolitical projection.

Brazil continues with its Drex pilot. The Central Bank is refining the technical design and expanding integration with Pix and tokenized asset projects. The country positions itself as a laboratory for hybrid rails, public and private.

The result is a mosaic of sovereign digital currencies, each with its own rhythm and architecture, all coexisting with global private stablecoins. Fragmentation is inevitable. Political time can never match the speed of code.

While SWIFT struggles to update a messaging standard, each nation is trying to reinvent its own money.

The rails of crypto settlement

While SWIFT sends messages, the new system moves real money. Settlement is no longer a promise; it is a continuous operation.

Bitcoin, Ethereum, and Solana form the rails of this global circuit. Each one serves a specific role within the new programmable liquidity framework.

Bitcoin is the neutral collateral. It has no liability, no central issuer, and cannot be inflated by decree. Since the approval of spot ETFs in the United States, the asset has entered the traditional financial system for good.

By October 2025, the combined AUM of Bitcoin ETFs stood between 150 and 170 billion dollars, with BlackRock’s IBIT alone near 100 billion. It is the institutionalization of an asset once considered marginal.

Ethereum is the dominant settlement layer. It hosts the leading stablecoins, tokenized real-world assets (RWAs), and staking contracts. It connects capital, network, and code, enabling the tokenization of everything from Treasury bills to money market funds.

Solana has become the high-frequency rail. Its performance has attracted flows from remittances and payment systems. The spot ETF approved in Hong Kong in October 2025 marked the network’s institutional entry. It is the closest experiment to a programmable global micropayment network.

Together, these three layers form the architecture of crypto settlement. While SWIFT sends messages between banks, code now settles, records, and audits in seconds. Settlement has left the hands of banks and entered the hands of code.

Who loses, who wins

Every infrastructure shift is, above all, a redistribution of margins. On-chain settlement merges authorization and payment into a single act.

What once required multiple intermediaries now happens in seconds at near-zero cost. The result is a structural compression for companies that profited from friction.

Visa, Mastercard, and SWIFT sit at the center of this shock. The business model that secured decades of profit relied on fees for processing, acquiring, and reconciliation.

When code performs all these steps automatically, the margin disappears. Consulting firms such as McKinsey and several industry reports already describe 2025 as the inflection point for payment infrastructure.

SWIFT is rushing to adopt ISO 20022 and launch new services, but it remains only messaging, not settlement.

At the same time, new winners are emerging. Coinbase captures institutional custody and fiat-on-chain conversion. Block (Square) builds on the Lightning Network and alternative rails. PayPal operates PYUSD and integrates crypto payments at commercial scale. Wise monetizes cross-border transfers outside of SWIFT, exploiting the efficiency gap.

In the tokenization arena, momentum is building as well. BlackRock’s BUIDL tokenized fund surpassed 1 billion dollars in 2025. Ondo Finance, through OUSG and USDY, expanded the tokenized Treasury market, now totaling 7 to 8.4 billion dollars.

Each new on-chain settlement removes a fee from the past and transfers efficiency to the future. It is the most profound reconfiguration in the modern history of payments.

The global test of trust

The new system has already won on efficiency. What remains is trust. Programmable settlement delivers speed, transparency, and near-zero cost, but it still operates on fragile layers of user experience and perceived security. This is the point where technology meets psychology.

The most visible risk is a run on stablecoins. If confidence falls and mass redemptions occur, issuers will be forced to sell T-bills, driving yields higher and disrupting U.S. Treasury financing.

Reuters and JPMorgan have already warned of this side effect: the larger stablecoins grow, the greater the risk of an inverted squeeze. Regulatory risk also looms.

Rule changes in the United States and Europe could reshape the entire economics of issuance and usage.

There is also usability risk. Interface failures, phishing, and private-key loss remain barriers to mass adoption.

The European Central Bank has already contracted anti-fraud technology for the digital euro, a sign that even central banks recognize the problem.

Despite the risks, the direction is irreversible. SWIFT is now the portrait of a system that requires intermediaries to exist. Code does the opposite. It removes the intermediary, records truth, and executes alone.

The new system will have no headquarters. It will have code.

Stablecoins and CBDCs buy time and control, not balance. The Treasury remains funded by tokenized private demand. SWIFT still sends messages. Programmable settlement already sends the future.

👉 If this lens helped you see the map more clearly, stay with us. Subscribe to The Black Line for essays, notes, and signals that track where power and price move next.

Good breakdown. The framing of stablecoins as unauthorized digital dollars and the Treasury as their indirect beneficiary was an interesting take that gave me a different perspective. Also, what struck me is your line about code replacing headquarters. It would represent a structural shift from institutional trust to programmable trust. I wonder how much puhback will occur.

Stablecoins will ensure continued USD dominance in a world where countries gradually shift away from using the USD for trade.